![[cover image]](images/issue/WR201710.jpg)

![[PDF]](images/pdf.gif)

Pay settlements stuck in rut as overall rise is 2.0% once again

Twelve months ago Workplace Report found that, apart from an expansion in bargaining around low pay, settlements seemed to be stuck in a 2.0% rut.

At first glance the 2016-17 pay round looks like another repeat with a median of 2.0%, public sector settlements clustered around 1.0%, and a slight lead for the private sector on 2.2%.

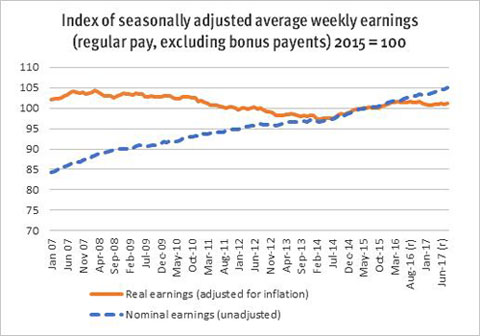

Pay settlements in the unionised labour market — the main focus of the LRD Pay Survey — are not the same as the growth in Average Weekly Earnings but, on both counts, living standards are at risk. At constant 2015 prices, average regular pay (excluding bonuses) is still lower than it was in March 2008).

TUC general secretary Frances O’Grady said: “The squeeze on living standards is not letting up. Ministers need to stop twiddling their thumbs and get wages rising across the economy”.

The TUC’s worries are shared by the Organisation for Economic Cooperation and Development, which recently warned about the downward trend in UK real wages. Reviving productivity growth is seen as key to ensuring higher living standards but Brexit uncertainty is “compounding the productivity challenge”.

The International Labour Organisation (ILO) has gone a step further: director general Guy Ryder argues that social dialogue and collective bargaining are “essential factors to promote inclusive growth”.

To explore this apparently sluggish growth in median pay rises Workplace Report this year includes an analysis of post-recession settlements using a sub-set of larger agreements for which LRD Payline records are most complete.

It points to much greater variation in pay settlements at the level of individual agreements than the overall pay medians. It could be seen as evidence of how negotiators might respond, given falling unemployment, skills shortages and the rising cost of living, if uncertainties are removed and collective bargaining is given a chance.

The 2016-17 Pay Survey

This year’s LRD Pay Survey draws on 927 separate pay settlements effective between 1 August 2016 and 31 July 2017. The median pay rise on lowest basic rates was 2.0% with the middle half of agreements falling between 1.25% and 2.74%. Weighted by the number of workers covered the median is a little higher at 2.4%.

Median increases in 2016-17 pay round

| Median lowest basic increase (%) | Median standard increase (%) | |||

|---|---|---|---|---|

| unweighted | weighted | unweighted | weighted | |

| Whole survey | 2.00% | 2.40% | 2.00% | 1.00% |

| Private sector | 2.20% | 2.50% | 2.00% | 2.50% |

| Public sector | 1.00% | 1.00% | 1.00% | 1.00% |

In the private sector, where the bulk of deals in the LRD Pay Survey apply, the median lowest basic increase was 2.2%, with half of all deals worth between 1.8% and 3.0%. The weighted median was 2.5%.

But in the public sector, where the government pay cap and austerity set the parameters, the median was 1.0% and the middle half of settlements were worth between zero and 2.2% (the latter being the increase at publicly-owned Network Rail).

Pay Review Body awards played a key role in these figures.

Pay Review Body settlements in 2016-17 pay round

Almost half of the public sector workforce, 2.4 million workers, have their pay set by government in the light of recommendations made by eight Pay Review Bodies, covering 45% of the public sector workforce and just over 60% of the pay bill. Five of the latest reports (which were delayed, partly by the June General Election) affected the 2016-17 pay round.

The reports reveal some of the stresses and strains arising from government pay restraint and the average 1% funding pay cap. There are problems arising from statutory and voluntary minimum wages, take-home pay/pension contributions, morale, recruitment and retention, pay structures for specific groups; and regional variations in the NHS.

The pay review bodies for school teachers and police have already released 2017-18 reports and they were respectively reported on in the July and September issues of Workplace Report. The 2017-18 report for the National Crime Agency was delayed and a new remit letter was issued on 18 October.

NHS Pay Review Body (1 April 2017)

The NHSPRB covers 1.36 million workers with a pay bill of £44 billion. It recommended a 1% increase on Agenda for Change pay points and High Cost Area payments, with Pay Point 1 in Northern Ireland adjusted to be above the level of the 2017-18 Living Wage. The UK and Welsh governments accepted the recommendations as did the Scottish government, whose separate recommendations apply alongside its own pay policy (£400 minimum increase for all staff whose full-time equivalent basic salary is £22,000 or less). A response in Northern Ireland has been delayed.

The review body also called for action to ensure that pay awards don’t cause staff to cross pension contribution thresholds, reducing take-home pay; improved evidence/data on take-home pay, pay bill trends and agency expenditure/use; action on productivity; attention to the implementation and effects of the National Living Wage and voluntary Living Wage; and flexibility to manage an exit from current pay policy. It expressed concern about cost pressures arising from Scottish government pay policy; flexibility in approving recruitment and retention premia; dissatisfaction and increasing leaving rates among Scotland’s ambulance staff; staff motivation; and a medium-term approach to pay.

Doctors and Dentists (1 April 2017)

DDRB recommendations cover 215,000 staff with a £19 billion pay bill. The review body recommended a 1% increase on national salary scales; on pay net of expenses for general practitioners; and on consultant performance awards (which the Scottish government did not accept). Recommendations were accepted (but delayed in Northern Ireland).

School Teachers (1 September 2016)

The STRB makes recommendations for England and Wales covering 308,000 staff with a pay bill of £14 billion. For the 2016-17 pay round a 1% increase applied to the minima and maxima of all classroom teachers and leadership pay ranges.

Armed Forces (1 April 2017)

AFPRB recommendations cover 168,000 staff with an annual pay bill of £9 billion. The review body recommended a 1% increase in base pay and on most recruitment and retention payments; other allowances; and on most accommodation charges (but not the daily food charge). It also recommended pay structure changes affecting Officer Aircrew and Army Non-Commissioned Officers and Weapons Engineering Submariners. These recommendations were accepted together with 1% for Service Medical and Dental Officers’ pay.

Police (1 September 2016)

The PRRB covers 133,000 staff in England, Wales and Northern Ireland with a pay bill of £7 billion. For 2016-17 there was a 1% consolidated increase that also applied to the Dog Handlers allowance and London Weighting, while South East allowance maxima increased to £2,000 or £3,000 depending on location. For 2017-18 the review body recommended a 2% increase consolidated to all pay points, London Weighting and Dog Handlers’ Allowance. It also called for specific local pay flexibility for chief officers and an integrated workforce and pay reform plan. The government responded with a 1% consolidated increase and an additional one-off non-consolidated payment to officers at federated and superintending ranks. A separate Northern Ireland report was submitted.

Prison Service (1 April 2017)

The PSPRB covers 25,000 staff in England, Wales and Northern Ireland with a pay bill of £900 million. Its recommendations for England and Wales, which were accepted in full, took account of the division of the workforce between open Fair and Sustainable (F&S) pay scales and closed grades.

The settlement involved a consolidated £400 increase to all F&S Band 2 to 5 pay points and closed officer and support grade equivalents, with the F&S Band 2 scale reduced to a two-point scale; and a consolidated 1% increase to Bands 7 to 11 open pay range maxima and minima and closed grade equivalents, including the closed grade hours addition. The Prison auxiliary spot rate increased to £15,575 and the night patrol spot rate to £17,575 while F&S operational graduate pay rates increased by £400.

Staff in Bands 2 to 5 progress by one pay point (unless on formal poor performance procedures) with a 1% non-consolidated payment for Staff in Band 5 who receive an ‘Outstanding’ performance marking. There was also progression in the open Band 7 to 11 pay ranges of between 4% and 6% dependent on performance marking.

The London fixed cash differential increased by 1%; the £5 increase an hour to Payment Plus, OSG overtime and Tornado was extended; and base pay on temporary promotion/cover should be the greater of either the minimum for the role or 5% of annual salary (and pensionable). Integration of the various different pay structures, allowance and supplements is to be considered in 2019.

Senior Salaries (1 April 2017)

The SSRB covers up to 5,000 judicial and senior military, civil service, NHS and police staff with a pay bill of around £600 million. Its main pay recommendations, which were accepted (but are outstanding in Northern Ireland), were to use in full the 1% available for basic pay increases. It was also asked to review the judicial salary structure.

National Crime Agency (1 August 2016)

NCARRB recommendations cover 1,900 full-time equivalent staff with a pay bill of £116 million. For 2016-17 a 1% award applied to pay range minima, maxima and target rates

Increase on lowest pay rates

Increases in the statutory National Living Wage and the voluntary Living Wage are still helping to push up some of the lowest pay rates. The National Living Wage currently equates to 55% of median earnings but is due to rise to 60% by 2020.

Meanwhile, the influence of the voluntary Living Wage continues to grow and there are now 3,500 accredited employers.

These statutory and voluntary minimums generated pressure for increases of more than 2% during the 2016-17 pay round. The NLW for workers aged 25 and over rose to £7.50 in April, a 4.71% increase on the April 2016 rate of £7.20.

The younger age-related minima increased last October as well as in April. The 21 to 24 National Minimum Wage rose to £7.05 from April 2017, a 1.44% increase on the October 2016 rate (£6.95), but a 3.73% total increase on the October 2015 rate (£6.70). The 18-20 NMW rose to £5.60 from April 2017, a 0.9% increase on the October 2016 rate (£5.55), but a 5.66% total increase from £5.30.

The under 18 NMW rose to £4.05 from April 2017, a 1.25% increase on the October 2016 rate (£4.00) and a 4.65% total increase from £3.87. The apprentice NMW rose to £3.50 from April 2017, a 2.94% increase on the October 2016 rate (£3.40) and a 6.06% total increase from £3.30.

The main voluntary Living Wage rate rose to £8.45 from November 2016, a 2.4% increase on the November 2015 rate (£8.25). The London Living Wage rose to £9.75 from November 2016, a 3.7% increase on the November 2015 rate (£9.40).

Standard increase

With rising statutory and voluntary minimum wage levels there is greater potential for lowest basic rates to change by a different percentage than rates payable to most grades or workers, what we call the “standard increase”.

Across the survey as a whole, the median standard increase at 2.0% was no different from the lowest basic median, but the middle half of all deals had a slightly lower value, between 1.0% and 2.5%. Weighted standard figures were much lower — with a median of 1.0% — while half of all increases were between 1.0% and 1.10% (reflecting big public sector deals).

Standard increases were higher in the private sector where more than a third of deals (37%) had an increase of 2.5% or more. Standard increases of 5% or more applied at a number of agreements including First Tram Operations in London (where drivers’ pay increased to £40,000, an 8.52% increase).

At Virgin Atlantic, there was a 6.65% increase for cabin crew and 4.45% for flight service managers and cabin service supervisors. At Rudolph & Hellmann Automotive, there was a 5% increase to all pay rates, including overtime.

The Film Artistes Association/PACT three-year deal provides an initial increase worth 5% (compared with the previously-agreed 2014 rates), while horseracing’s Stable Staff national agreement provided a 5.5% increase in October 2016.

Inflation

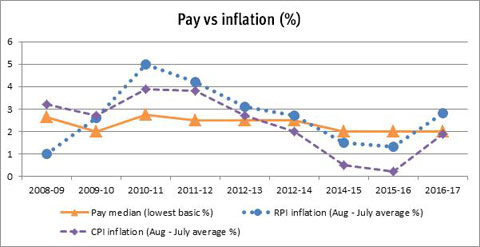

The latest figures for September show retail prices rising at a rate of 3.9% as measured by the Retail Prices Index or 3.0% on the Consumer Prices Index (CPI), so the squeeze on pay and earnings is back on.

Averaged over 2016-17 pay round the figures were 2.8% RPI and 1.9% CPI. RPI figures are increasingly ignored by the media yet were still explicitly referred to in over 6% of all pay deals in this year’s LRD Pay Survey, compared with just 1.9% that mention the CPI.

Long-term deals

One in five pay deals in the survey run for 24 months. However, some are even longer-term, setting pay for three or four years or more, proving that negotiators have not lost their appetite for the predictability of deals that stretch over two or more pay rounds.

Among the newest longer-term deals, the Electrical Contracting JIB and its Scottish counterpart agreed an initial increase of 2.0%, while drivers at GTR Thameslink Great Northern received 2.3% (taking their salary to £52,174 from October 2016). Just into its second year, the deal at Multi Packaging Solutions (Leicester) was a flat-rate £15 a week increase, worth 4.8% on the lowest basic rate.

Staff at Oxford City Council entered their fifth and final year with a 1.5% increase adn pay starting at £9.49 an hour (the Oxford Living Wage is £9.26 an hour).

Meanwhile, Spirit Aerosystems is half way through a 10-year agreement based on average CPI inflation, but with a 1% underpin.

The large Department for Work and Pensions bargaining group for AA to HEO grades is also in the midst of a four-year deal. No individual is to receive less than 1.1% each year subject to satisfactory performance (nor more than 5% unless linked to a statutory increase). Staff on their pay scale minima get the highest increases of between 1.1% and 5%.

The table on page 17 reveals that some industrial sectors had slightly higher median settlement levels, including transport and communications, engineering and metal products, and “other manufacturing”, such as food and drink.

Public administration had a 3.4% weighted lowest basic increase (simply because of at the increase at the bottom of the local government NJC pay spine).

Retail, wholesale, hotels & catering had a relatively high increase of 2.5% but the weighted increase was lower at 1.72%. In health, the median was 1.25% while in education the weighted median (reflecting larger deals) was 1.0%.

Pay post-recession

For this year’s LRD Pay Survey, Workplace Report has taken a retrospective look at around 90 large collective agreements (covering 500 or more workers) whose annual pay rises can be in most cases be tracked back to 2008-09. It includes all the broad industrial sectors and has allowed the calculation of long-term average increases, and an assessment of the variability between the lowest and highest deals.

On this basis, annual settlements averaged out at 2.47% on the lowest basic rate and 2.05% on the standard increase, consistent with successive LRD Pay Survey medians which have mostly been worth 2.0% to 2.5% since the recession (see chart).

Turning to the important question of responsiveness or variability, the difference between the smallest lowest-basic-rate increase and the largest, among individual settlements, averaged out at 4.3 percentage points.

Looking at the standard increase, which is more reflective of the rise for most grades or workers, the difference between the smallest and largest annual increases averaged out at 3.0 percentage points, more than value of one average annual pay rise.

Among this set of agreements, the widest gap between the smallest lowest-basic-rate increase (including pay freezes) and the largest was over 10 percentage points. The widest gap between the smallest standard increase and the largest was over 7 percentage points. Clearly there is a lot going on behind apparently stable LRD Pay Survey medians.

Increases by industrial sector

Median increases in 2016-17 pay round by industrial sector

| Median lowest basic inrease (%) | Median standard increase (%) | |||

|---|---|---|---|---|

| unweighted | weighted | unweighted | weighted | |

| Retail, wholesale, hotels & catering | 2.50% | 1.72% | 2.50% | 0.00% |

| Manufacturing - engieering & metal products | 2.30% | 2.50% | 2.35% | 2.50% |

| Manufacturing - other sectors | 2.23% | 2.32% | 2.00% | 2.30% |

| Transport & communication | 2.20% | 2.20% | 2.20% | 2.20% |

| Construction | 2.00% | 2.75% | 2.00% | 2.75% |

| Other services | 2.00% | 2.42% | 1.50% | 1.50% |

| Energy, water, mining, nuclear | 2.00% | 2.20% | 2.00% | 2.20% |

| Manufacturing - chemical, mineral, metals | 2.00% | 2.00% | 2.00% | 2.00% |

| Finance & business services | 2.00% | 2.00% | 2.00% | 2.50% |

| Public administration | 1.25% | 3.40% | 1.00% | 1.00% |

| Health | 1.25% | 1.00% | 1.00% | 1.00% |

| Education | 0.00% | 1.00% | 0.00% | 1.00% |

Agriculture

Most agricultural workers — the 300,000 in England — no longer have the protection of a national pay agreement, but sectoral minimum wage setting arrangements survive in Scotland, Northern Ireland and Wales. Following a 2015 review, the Scottish Rural Affairs Secretary said the evidence in favour of retaining the Wages Board was “compelling” (even though Scottish farm employers seem to disagree).

Under the Agricultural Wages Order (Scotland), the new minimum hourly rate of £7.50 is payable to all, regardless of age or period of time worked for the same employer, an effective pay rise of 7.91%. It pays £8.64 for workers who have been with the same employer for over 26 weeks who hold a qualification, and apprentices £4.14. Since 2008-09, increases have ranged from 4%, 3% and 2.5% to 1.2%, but the latest 7.91% rise emphasises the responsiveness of this negotiated statutory framework.

Energy, water, mining

The lowest basic rate median increase in 2016-17 was 2.0%. Offshore Divers have one of the highest average settlement levels in the sector (3.95%) but also the biggest gap between their 2011-12 high-point (7.1%) and the current two-year pay freeze.

Western Power Distribution has seen average pay rises of around 3.8% since the recession, but recent deals have been lower. Its second-year increase in April was based on average RPI for July-December 2016 (2.07%) plus 0.5%, raising basic pay and allowances by 2.57%. The first-year increase (2.5%) was not inflation-linked — otherwise it might have been closer to 1%.

The latest pay round — 2016-17 — saw a return to 3%-plus pay rises for National Grid non-industrial staff, after lower RPI-based rises in 2014-15 and 2015-16. Its highest standard increase since the recession was 3.3% in 2012-13, its lowest 0.9% in 2014-15. Timing worked out well this year as the 3.1% increase from 1 July 2017 was based on the inflation rate for March 2017. It flowed through to allowances and included an important commitment to “no change” to the definition of pensionable pay.

Chemicals, minerals, metal

In chemicals, mineral and metal manufacturing the median in 2016-17 was 2.0%. That was the going rate in the latest pay deal at BASF Bradford. Before 2012-13 its pay deals were typically 3% to 4%, but the gap biggest gap between its lowest and highest post-recession settlements is 2.5 percentage points. Its 2013-16 deal reduced shift and multi-skill payments, adding the difference to base pay, showing how negotiators respond to changing circumstances.

Boots Contract Manufacturing has had a fairly steady run of 2.0% deals, but its latest rise came with a commitment to meaningful discussions around the grading structure (and followed a permanent change to the anniversary date). Pay increases at CF Fertilisers have been more varied, the highest 5.4% in 2010-11, the lowest 2.0% between 2015 and 2016. Its latest pay rise was 2.9% on all salaries and associated allowances.

Engineering & metal products

Engineering and metal products was one of the stronger sectors in the 2016-17 LRD Pay Survey with a median pay rise of 2.3%.

Bentley Motors (Crewe) agreed a deal which will see pay increase by 6.5% over three years, along with consolidated payments worth £900. Its effective value will be boosted by a reduction in the working week from 37 to 35 hours with no loss of pay from 1 January 2019. For the first year £250 was consolidated into basic pay and then a 2% increase applied. Since the recession Bentley has seen pay frozen but also, at the other end of the spectrum, had a 4.75% rise in 2011.

Since the end of the recession construction equipment group JCB has relied explicitly on the November increase in the Retail Prices Index as a guide to its settlements (which have ranged between 1.1% and 5.2%). The new three-year deal maintained that tradition, delivering a 2.2% pay increase (with a £400 Christmas Bonus also to be paid). Chief executive officer Graeme Macdonald said it gave “the stability we need to plan for 2017 and beyond as we seek to grow the business in the next few years”.

Other manufacturing

Pay deals in the “other manufacturing” sector in 2016-17 have been slightly ahead of the Pay Survey trend, on a median of 2.23%. At Mondelez (Cadbury), pay rises since the recession have been as high as 5.2% (2015), but more typically around 3%-4%. The new two-year deal continued that trend with a 3.2% increase from 1 March 2017 based on the RPI for February 2017.

Other large bargaining groups in the sector have seen less variation in their settlements. The agreed 2.32% pay increase at Kraft Heinz in January was based on the average RPI for September, October and November 2016 (2.07%) plus 0.25%, following a first-stage RPI-beating 1.6%, plus up to 4.99% bonus based on attendance. An important existing commitment to maintain negotiated terms and conditions for the duration of the pay deal was carried over from the previous 20-month pay deal, when large-scale job losses cut the workforce from 1,150 to 850.

Construction

Pay deals in the sector delivered a median increase of 2.0% in 2016-17.

Although a set of superficially similar national multi-employer deals dominate the sector, their settlement history varies.

The Construction Industry Joint Council(CIJC) had a 2.75% increase in basic rates this year in the third stage of a three-stage two-year agreement. Some allowances increased by 3.1% (due to an RPI inflation link) while annual leave increases and became more flexible. Over the previous four pay rounds, pay rises varied within a narrow range (between 2% and 3%) but followed a succession of post-recession pay freezes.

By contrast, the Engineering Construction (NAECI) NJC almost avoided pay freezes and some of its biggest pay rises came just after the recession. This year it entered the second stage a three-year deal with a 2% increase in hourly pay rates, travel and accommodation allowances (following a 1.5% increase last year).

Retail, wholesale etc

Settlements across the sector have been quite varied, due partly to the introduction of the National Living Wage. In 2016-17, the median lowest basic pay rise was 2.5%.

Two of the sector’s biggest employers, Tesco and Sainsbury’s, have agreed significant pay deals this year (see page 5), but so too did wholesaler Booker (which Tesco has been hoping to buy). Its Branch Assistant hourly rate increased to £7.60 in April, while location-based rates increased to £8.53 an hour (Inner London) and £8.17 (Outer/Hotspot). Booker’s lowest basic pay rises have ranged from 1.18% to 6.4% since the recession.

Transport and communications

Settlements were grouped strongly around a 2.2% median in the pay survey. There is a wide range of transport and communications deals in our post-recession analysis, as there is in the LRD Pay Survey as a whole. Some have seen differences of as much as four to six percentage points between their lowest and highest settlements, but for others the gap has been much smaller (a little as one percentage point).

At Eurostar International, the latest two-year deal involved a 1% increase on basic pay and job-related allowances plus a 3.2% increase to the Home to Work Travel allowance, enhanced overtime and joint reviews on sickness and absence policies, equal opportunities, diversity and family friendly/flexibility policies. It has had a varied pattern of higher and lower settlements since the recession.

So too has the now privatised Royal Mail where there have been both pay freezes and rises of up to 3.5%. The last pay rise was a 1.6% increase in April 2016, but a dispute over pay and pensions was developing as Workplace Report went to press.

Finance and business services

The sector had median pay rises of 2.0% in the survey but many employers negotiate on a pay bill and performance pay basis, making it difficult to compare their settlements or count them in the survey.

Barclays Bank is an example but its pattern of pay pot increases has varied, ranging from 5.0% in 2009 to a negotiated 2.0% (when the RPI-linked formula would have delivered no increase), 2.3%, 2.5%, 2.4%, 3.0%, 2.3% and 2.1%. Its new three-year deal began with a 2.5% increase in salary spend plus new grade minima set at 90% of relevant market medians. Other changes included its Living Wage arrangements.

At Diligenta, a subsidiary of Tata Consultancy Services, there was a backdated across-the-board increase of 2.25% with no variable or performance-related elements at its UK Life Services group.

Across the board increases have applied in previous years (usually similar to the overall settlement trend), sometimes with a small percentage for discretionary performance-related awards - but not this year. Extra percentage increases for staff paid less than £14,000-£15,000 were included in the previous two deals, but the latest deal effectively established the voluntary Living Wage as a minimum.

Public administration

Pay medians in public administration are a standard 1.0%, but with a much higher 3.4% on the weighted lowest basic rate median. That simply reflects minimum pay point increases in the Local Government Services NJC agreement for England, Wales and Northern Ireland.

Under the second year of its two-year deal there was a 1% increase on pay points from spinal column point 17 and above (from 1 April 2017) with higher increases on the lower pay points up to 3.4%. Looking back, earlier pay freezes combined with measures to help the lowest paid mean that its average standard has been 0.69% but lowest basic increases have been higher at 2.08%.

At HM Revenue and Customs, pay awards continue to be capped by the Treasury at 1% of pay bill. In June an imposed deal paid a flat rate consolidated award of 0.8% of the 2016 maximum of each pay range. Pay range minimums increase by between 0.89% and 1.2%; maximums increased by just over 0.8% (but with an exception for some fast stream staff, and a 0.4% non-consolidated fund for staff with “exceeded” performance ratings). Over the years its lowest basic rate increases have ranged from zero to 5.97%.

Education

The weighted settlement median in the education sector, which is dominated by a small number of large national agreements (and one pay review body, see page 00), is 1.0%.

The Higher Education JNC made two adjustments to pay during the 2016-17 pay round, starting with an imposed 1.1% increase, but with higher increases for the lowest seven points on the pay scale. Then, from the 1 April 2017, scale point 1 was removed, with staff uplifted to scale point 2. For the lowest paid, these two steps amounted to a 5.09% increase for the year. It tops earlier lowest basic rate increases, but back in 2008-09 an RPI-based increase was worth 5.0%.

The Sixth Form Colleges are covered by two collective agreements, one for teachers and the other for support staff. Both have seen variation in their lowest-basic-rate settlements since the recession. For support staff that trend continued in 2016-17 with a 1% increase to all pay points from 1 September 2016 and a second stage in January that deleted the bottom three points of the pay scale, giving a 6.39% overall increase for those on the lowest pay.

Health and social work

This sector saw a 1.25% median increase. The sector is dominated by two NHS pay review bodies (see page 19), but also includes the JNC for youth and community workers. Its September 2016 agreement raised most pay points by 1%, but deleted point 1 and applied increases worth between 1.2% and 2.0% to points 2 to 5. The resulting 6.23% rise is the largest lowest basic rate increase since the recession.

Other services

The “other services”’ sector is as diverse as its settlements. The British Library saw a 2.04% pay bill increase from the 1 August 2016. The pay matrix applied a 3% increase to the Grade ELA South minimum salary, alongside performance pay and a commitment to the Living Wage. Long-term variations in its settlements have mainly focussed on the lowest pay rates.

The national agreement for UK Theatres included an increase for Grades 4 and 5 staff to the new National Minimum Wage (a 4.2% increase) in April along with a 4.2% increase for Grade 3 and 2% for Grades 1 and 2.

The full LRD Pay Survey is available at www.lrd.org.uk/index.php?pagid=102